April marks the start of the busy season in real estate. If you are considering buying or selling there are four points to keep in mind about the 2025 spring market.

Continued Price Appreciation. Home prices are still on the rise. The increases are less significant than in prior years. This moderate appreciation may ease the concerns of potential buyers. It suggests improvements in inventory and affordability.

Varying Mortgage Rates. With mortgage rate fluctuations, it is a good idea to consult a mortgage consultant sooner rather than later. Thirty-year rates have remained below 7% almost all year. Locking in a rate now can be beneficial for your long-term plans.

Example:

At a 3% interest rate: For a $300,000 mortgage, a 30-year loan would cost about $1,265 a month.

At a 6% interest rate: The same mortgage would increase to roughly $1,798 a month.

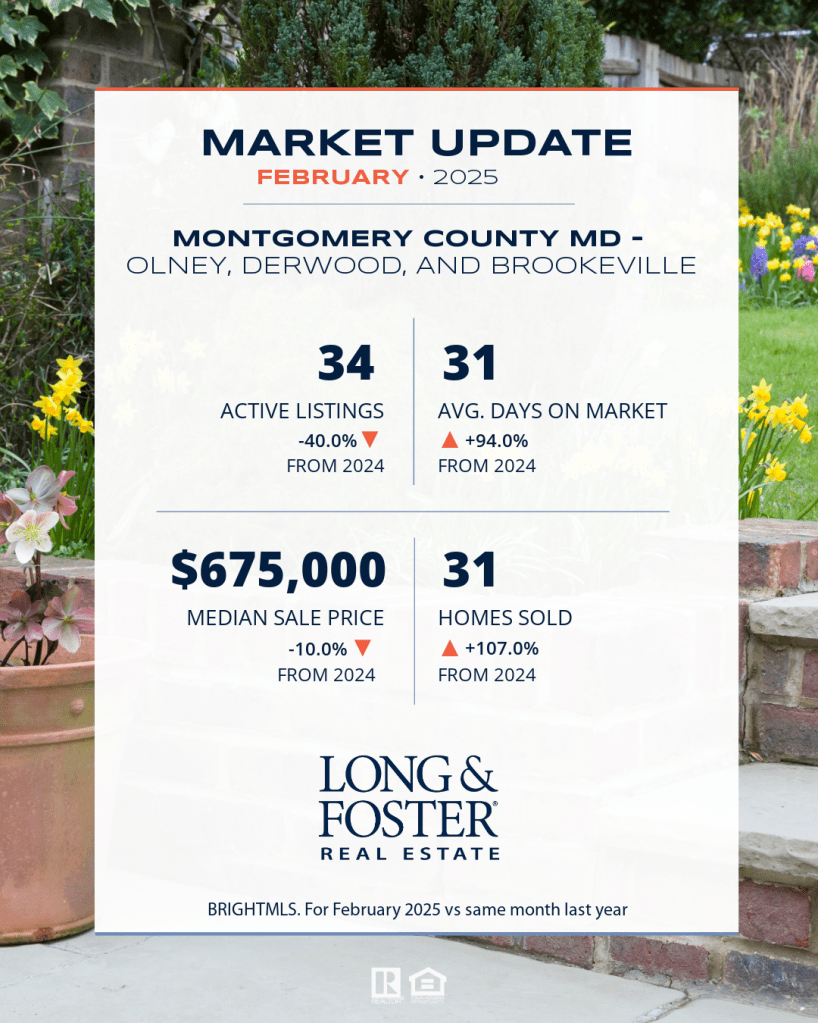

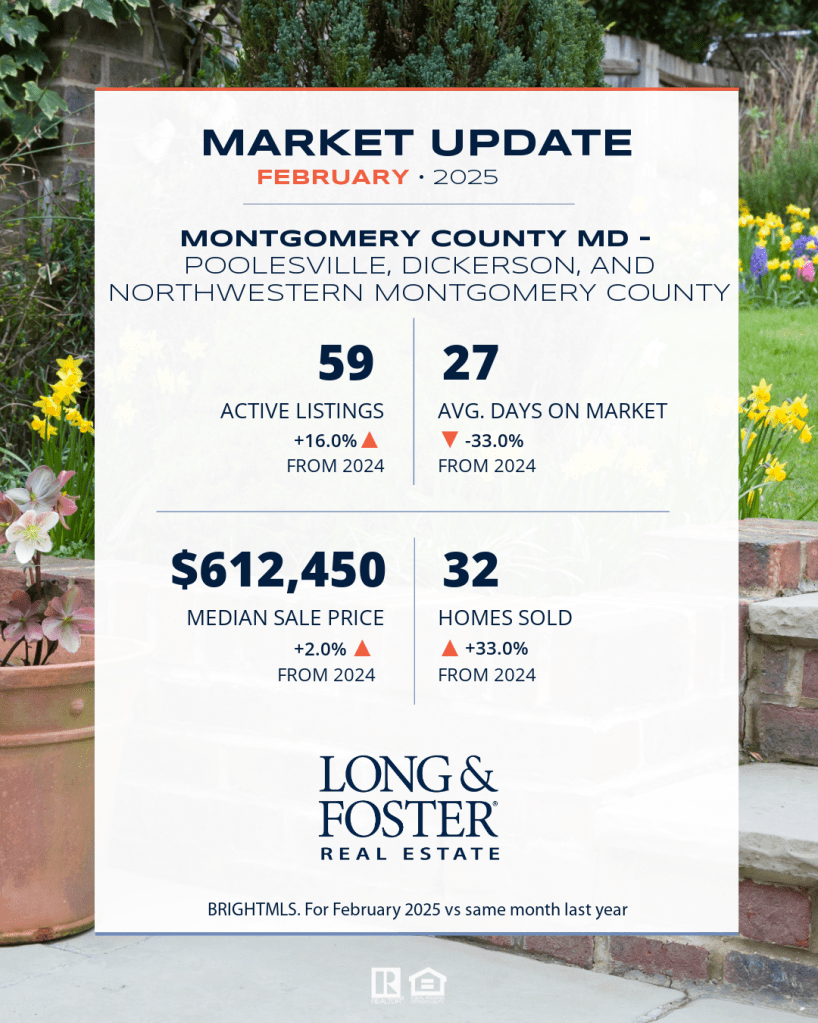

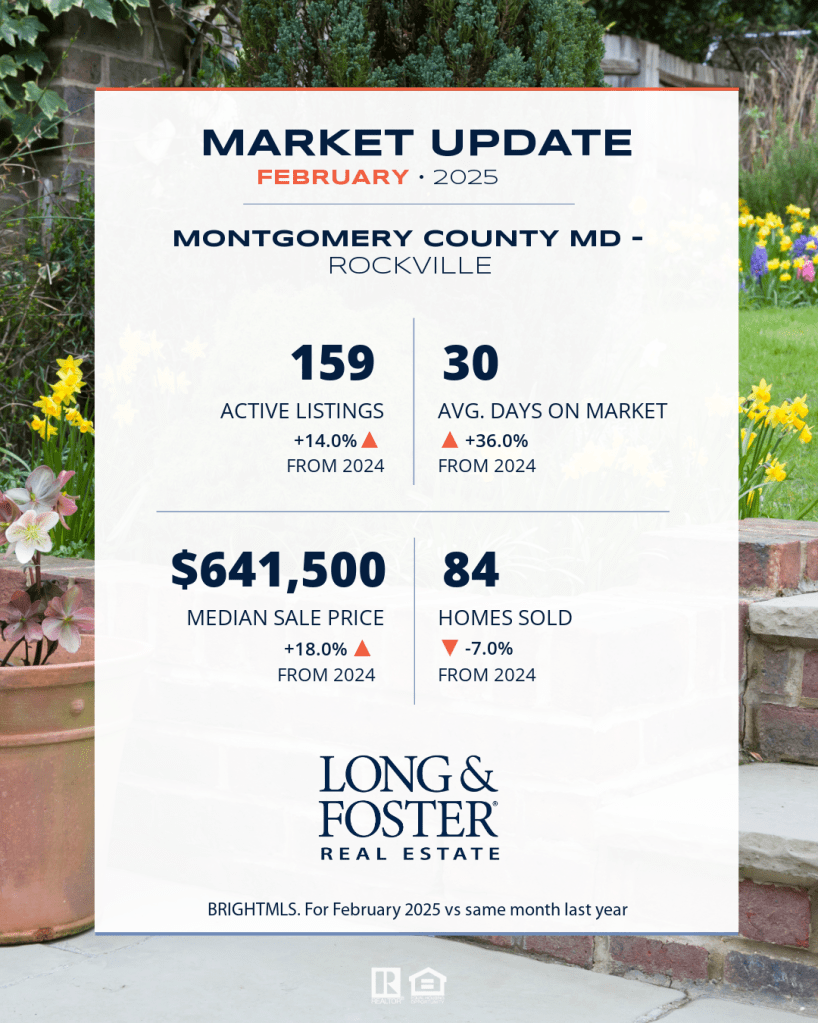

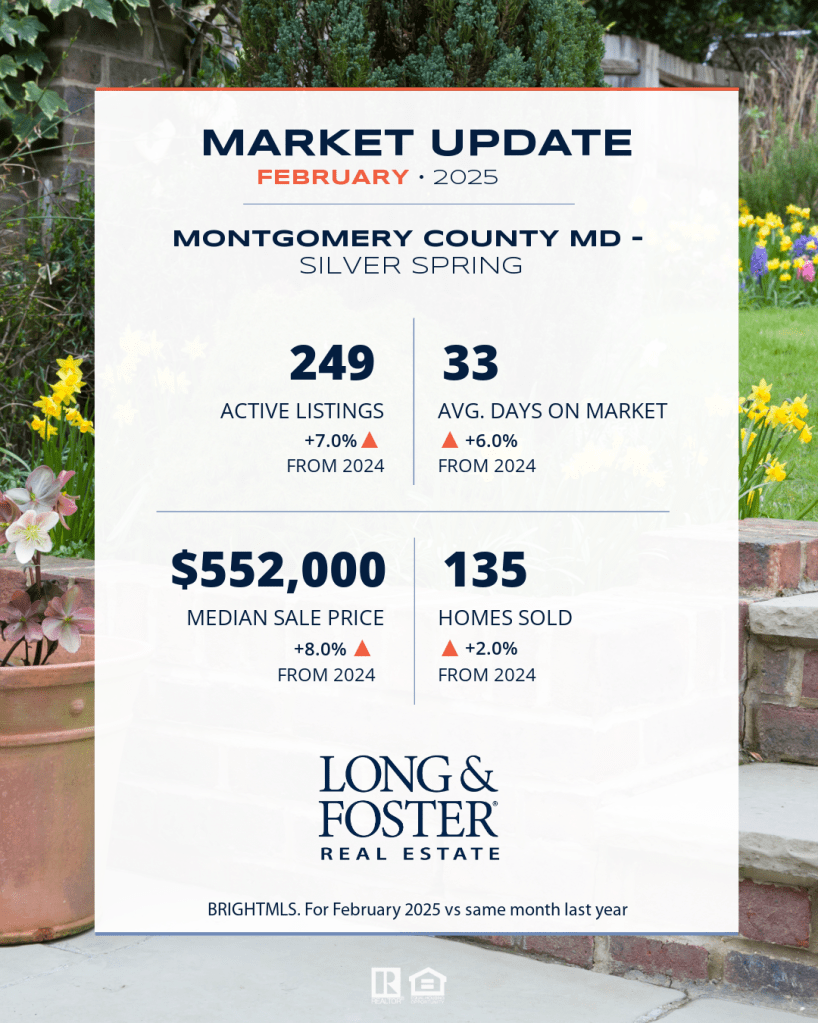

Growing Inventory. Real estate conditions vary by location. There is an increase in the number of homes for sale in parts of the Mid-Atlantic and Northeast. If you’re interested in a specific market, please reach out. I can track inventory levels and keep you updated on any listed properties that meet your needs.

Balanced Market. For the first time in years, experts predict a balanced market in 2025. This shift benefits both buyers and sellers after a long period during the pandemic when the market was dominated by sellers.

Real estate trends vary significantly from one area to another. If you would like more details about our local community, feel free to contact me. I am happy to provide a competitive market analysisfor your home or share insights from our local market reports.

Plus, if you are house-hunting, consider attending Long & Foster’s Open House Weekend on April 26 and 27. You can find open houses near you here. Wishing you a happy spring.

A mortgage is a type of loan used to purchase a home or property. When you take out a mortgage, you borrow money from a lender to cover the cost of the property. In return, you agree to pay the lender back over a set period of time.

How a Mortgage Works:

Loan Amount: The amount you borrow from the lender.

Down Payment: You typically pay part of the property’s price upfront. This is usually 5% to 20% of the home’s price. This is called a down payment.

Interest Rate: The rate at which the lender charges you interest on the loan, which affects your monthly payments.

Monthly Payments: You will make regular payments to the lender. These payments typically cover the loan’s principal (the amount you borrowed) and interest.

Collateral: The property you are buying acts as collateral. If you fail to make payments, the lender can take possession of the property through foreclosure.

How to Get a Mortgage:

Check Your Credit Score: Lenders use your credit score to determine your mortgage eligibility. It also affects what interest rate you get. A higher credit score generally leads to better loan terms.

Determine Your Budget: Figure out how much house you can afford based on your income, debt, and expenses. A common rule is that your monthly housing costs should not exceed 28-30% of your gross monthly income.

Save for a Down Payment: Most lenders require a down payment of at least 5-20% of the home price. The larger your down payment, the better your loan terms will be.

Choose a Lender: Shop around for mortgage lenders (banks, credit unions, online lenders) to compare interest rates and terms.

Get Pre-Approved: Getting pre-approved means the lender will review your financials (credit, income, assets, etc.) to determine how much they’re willing to lend you.

Submit an Application: Once you choose a lender, you will submit a formal application. You need to provide details about your finances and the property you’re purchasing.

Home Appraisal: The lender will require an appraisal to determine the home’s market value.

Loan Approval and Closing: If your loan is approved, you will sign the necessary documents. You will then close on the property. This process officially transfers ownership.

Once the mortgage is approved, the property becomes yours. You will start making regular payments as outlined in your loan agreement.

Would you like more details on any specific part of this process? Would you like to get started with a mortgage company? This company was ranked #1 in consumer satisfaction by JD Power last year.

Start here, and the first client of mine to close this spring will receive a $500 credit towards closing costs.

Credit scores are used in the US to assess if a person will pay debts. This score is important if you are interested in purchasing or renting a property.

Loan Approval: Lenders use your credit score to evaluate your risk as a borrower. A high credit score suggests you are unlikely to default on payments. This makes lenders more willing to approve you for a mortgage. A low score can make it harder to get approved, especially for traditional loans.

Interest Rates: If you are approved for a loan or mortgage, a high score results in a low interest rate. This saves you thousands of dollars over the life of a loan.

Renting in Competitive Markets: In cities with limited housing availability, it is easier to rent with a high credit score.

What is a good credit score?

A “good” credit score can vary slightly depending on the scoring model used but generally speaking:

Excellent: 750–850

Good: 700–749

Fair: 650–699

Poor: 300–649

If you want the best mortgage or loan offers, a score of 740 or higher is ideal. Scores in the “fair” range can still get you approved, but the terms are unlikely to be as favorable.

How can you improve your credit score?

Improving your credit score takes time, but with consistent effort, you can boost your score. Here are some effective strategies to help you improve your credit:

1. Pay Your Bills on Time

Payment history is the biggest factor in your credit score. Always pay your credit cards, loans, and other bills on time. Even one missed payment can significantly impact your score.

2. Reduce Credit Card Balances

Try to keep your credit utilization ratio below 30%. For example, if your credit limit is $1,000, try to keep your balance under $300. The lower your balance, the better it is for your score.

3. Avoid Opening Too Many New Accounts

Each time you apply for a credit card or loan, it results in a hard inquiry. This temporarily lowers your score. Try to limit the number of new accounts you open.

4. Check Your Credit Report for Errors

Errors on your credit report can drag down your score. Obtain your free credit report once a year from Equifax, Experian, and TransUnion to check for inaccuracies. Dispute any incorrect information.

5. Settle Outstanding Debts

If you have any outstanding collections, try to pay them off or settle them. Some lenders are willing to remove a collection entry from your credit report if you settle the debt.

6. Keep Old Accounts Open

Length of credit history: Keeping old accounts open can help improve your score by showing a longer credit history. Just make sure not to incur any fees for maintaining these accounts.

7. Diversify Your Credit

A mix of credit types (credit cards, car loans, mortgages, etc.) can help your score. However, only take on new debt if you can manage it responsibly—don’t open unnecessary accounts just to diversify.

8. Pay More Than the Minimum on Credit Cards

Paying more than the minimum will reduce your debt faster and lower your credit utilization ratio.

9. Consider a Secured Credit Card

If you have limited credit history or a low score, applying for a secured credit card. This can be a good way to build or rebuild credit. With a secured card, you deposit an amount equal to your credit limit. Your responsible usage will be reported to the credit bureaus.

Improving your credit score is a gradual process. While results take time, these steps will help set you on the right path. Keep monitoring your credit, and over time, your score will improve.

Tax season is fast approaching. If you purchased or sold a home last year, there are several tax benefits and rules that impact your return. Here are key tax details homeowners should keep in mind.

Home Mortgage Interest Deductions

One of the most common tax breaks for homeowners is the mortgage interest deduction. The amount you can deduct depends on when your mortgage was finalized:

Mortgages Closed Before December 16, 2017: You can deduct mortgage interest on a loan balance up to $1 million.

Mortgages Closed After December 16, 2017: The deduction limit drops to $750,000 for both primary residences and second homes.

Property Tax Deductions

You can deduct up to $10,000 for a combination of state and local property, income, and sales taxes. This applies to property taxes on your primary home, a vacation home, and even undeveloped land. Keep in mind that the $10,000 cap applies to all state and local taxes.

Mortgage Insurance Premiums

If you paid for private mortgage insurance (PMI) last year, you qualify for a deduction—depending on your income. PMI is required when you put down less than 20% on a home. This deduction provides some financial relief at tax time.

Capital Gains Tax Exclusions

If you sold your primary residence in 2024, you may be eligible for a capital gains tax exclusion. Married couples filing jointly can exclude up to $500,000 in capital gains. Single filers can exclude up to $250,000, if they lived in the home for two of the last five years. This can be a huge benefit for reducing your taxable income from the sale of your home.

Consult a Tax Professional

These are just a few of the housing-related tax benefits you can take advantage of. Keep in mind that tax laws can change and vary based on your personal circumstances. It is a good idea to consult with a tax advisor to get the full range of deductions available.

If you have any questions about real estate or need assistance, feel free to contact me.

Are you looking for a strategy to combat inflation while ensuring a steady cash flow? One option worth considering is investing in rental properties. Real estate has long been an attractive way to build wealth, offering numerous financial and tax benefits. In this post, we’ll break down the key advantages of owning rental properties and why they can be an excellent choice for long-term financial success.

1. Steady Cash Flow

One of the biggest financial benefits of owning rental properties is the ability to generate consistent, passive income. When managed well, rental properties can provide a steady cash flow month after month. Ideally, your rental income will exceed your expenses, leaving you with extra money that you can reinvest, save, or use to fund your lifestyle.

2. Property Appreciation

Over time, real estate tends to appreciate in value, especially if the property is located in a desirable area. While short-term fluctuations in the market can occur, historical trends show that real estate values generally rise over the long run. This appreciation can lead to significant gains when you sell the property, or it can increase your equity if you hold onto it.

3. A Hedge Against Inflation

Rental properties are a great way to hedge against inflation. As the cost of living increases, so do rents. This means that your rental income is likely to grow in line with, or even outpace, inflation. If your mortgage payment is fixed, this can create a significant advantage. As inflation rises, your rental income can increase, while your mortgage payment stays the same, boosting your cash flow in real terms.

4. Fixed-Rate Mortgages

If you have a fixed-rate mortgage, your monthly mortgage payment will remain consistent even as inflation increases. This can be especially advantageous during times of rising prices. Meanwhile, your rental income can grow as rents increase, meaning your overall financial situation improves. Essentially, your mortgage payment is locked in, while your rental income can rise, allowing you to enjoy greater profitability.

5. Tax Advantages of Rental Properties

One of the most significant advantages of owning rental property is the potential tax benefits. One such benefit is depreciation. Depreciation allows you to deduct the cost of the property’s building (excluding the land) over a period of time—27.5 years for residential properties and 39 years for commercial properties.

For example, let’s say you purchase a rental property for $300,000, and the land is worth $50,000. You could depreciate the building’s value of $250,000 over 27.5 years, resulting in an annual depreciation deduction of approximately $9,091. This deduction can help lower your taxable income, even if the property is appreciating in value.

In addition to depreciation, other deductible expenses include operating costs, property taxes, insurance, travel, and mileage. All of these factors combine to reduce your overall tax burden, making rental properties an attractive investment option. As always, it’s best to consult a tax professional to understand the specific tax advantages available to you.

6. Financing Options Based on Rental Income Potential

If you’re unsure about whether you can afford a mortgage for a rental property, you may be surprised to learn that there are financing options available that are based on the rental income potential of the property rather than your personal income. This can make it easier to invest in real estate, even if you don’t have a high income or extensive financial history. Speak with a real estate loan officer to explore your options and find out what financing solutions might work best for your situation. Get started on financing.

7. Partnering with a Real Estate Agent

Once you’ve decided that investing in rental properties is the right move for you, it’s time to shop for the perfect property. A local real estate agent can be an invaluable resource in facilitating the buying process. They can help you navigate the complexities of property transactions and ensure that everything goes smoothly, from the initial search to the final paperwork. Contact me to learn more.

Conclusion

Rental properties offer a range of financial and tax benefits that can help you build wealth, stay ahead of inflation, and generate steady cash flow. From appreciating property values to passive income and tax deductions, investing in real estate can be a powerful way to achieve your financial goals.

If you’re considering adding rental properties to your investment portfolio, now may be a great time to start. Be sure to consult with financial and tax professionals to ensure that you’re making the most informed decisions based on your unique circumstances. Happy investing.